ECONOMICS – IMPORTANT QUESTIONS BY KHALID AZIZ

Micro Economics 1) How indifference curve technique helps a consumer to achieve equilibrium position? Discuss properties of indifference curve. 2) Define perfect competition and explain its assumptions. Explain with help of a diagram a firm’s equilibrium condition in the short run, under perfect competition. 3) Price effect is the combination of income effect and substitution effect. Explain and illustrate. 4) Compare monopoly with monopolistic competition. Explain with the help of diagrams, the short run equilibrium of a firm under monopolistic competition. 5) Explain law of diminishing returns to scale. Why this law is important for agricultural sector? 6) Distinguish between micro and macro approach to economic analysis and also discuss the need for combining the two approaches. 7) Explain the concept of elasticity of demand. Differentiate between (i) Income elasticity of demand (ii) Price elasticity of demand (iii) Cross elasticity of demand 8) Write notes on a) Law of diminishing marginal utility. b) Internal & External Economies c) Laws of increasing & constant return to scale. d) Point & Arc elasticity of demand e) Change in quantity demanded and change in demand f) Price Discrimination g) Marginal cost and Average cost

Macro Economics 1) Differentiate between (i) GNP & GDP (ii) National income at market price and National income at factor cost. (iii) Personal income & Disposable income 2) Define National Income, what is the importance of study of national income? 3) Distinguish between consumption and consumption function. Explain the factors which determine the propensity to consume. 4) Distinguish between APS and MPS. What are the factors that determine saving in an economy? 5) Short notes a) Autonomous and Induced Investment b) Marginal efficiency of capital c) Multiplier d) Acceleration e) Objectives of fiscal policy f) Objectives of monetary policy g) Phases of trade cycle

Economic Systems 1) Give salient features of Islamic economic system and compare it with capitalism and socialism. 2) Explain the importance of zakat in the process of distribution of wealth in Islamic state.

Tuesday, December 31, 2013

Monday, December 30, 2013

B-COM PART 2: MANAGEMENT – IMPORTANT QUESTIONS BY KHALID AZIZ

MANAGEMENT – IMPORTANT QUESTIONS

BY KHALID AZIZ

1) Define management. State briefly the universal functions of a manager.

2) Define planning. Discuss briefly the various steps involved in planning.

3) Define staffing. Describe briefly the various steps involved in staffing.

4) Define groups. How they grow? And how they flow?

5) Explain policies, rules and procedures in detail.

6) Define decision making. State the guidelines of decision making. What is rational

decision making?

7) What is MBO? What are its characteristics and its objectives?

8) Define motivation and list various theories of motivation.

9) What is communication? What are the steps involved in communication? Briefly

state various barriers to communication.

10) Explain briefly the phases of control. State the characteristics of a good control

system.

11)Notes

a) Orientation & Training

b) William. G. Scot’s 4 pillars of organization

c) Budget & its types

d) Mc Gregor’s X & Y theory

e) Span of management

f) Hawthorn effect

g) Management audit

h) Henry Fayol’s 14 principles of management

i) Elton Mayo’s human relations theory

j) Role of Frederick. W. Taylor in management

k) Nominal group technique & Delphi technique

l) Abraham Maslow’s theory of humanistic approach about human need

m) 5 c’s of communication

n) Human balance sheet

Sunday, December 29, 2013

INTRODUCTION TO BUSINESS – IMPORTANT QUESTIONS BY KHALID AZIZ

INTRODUCTION TO BUSINESS – IMPORTANT QUESTIONS BY KHALID AZIZ

2) WHAT DO YOU MEAN BY BUSINESS PROBLEMS? LIST THE USUAL PROBLEMS OF BUSINESS.

3) WHAT ARE THE EFFECTS OF PRIVATIZATION OVER ECONOMY OF PAKISTAN?

4) DIFFERENTIATE BETWEEN CAPITALISM AND SOCIALISM. WHAT ECONOMIC SYSTEM HAS BEEN FOLLOWED IN PAKISTAN? WRITE A NOTE ON MIXED ECONOMY.

5) NAME VARIOUS ENVIRONMENTS INFLUENCE BUSINESS ACTIVITIES.DISCUSS SOCIAL AND CULTURAL ENVIRONMENT.

7) WHAT ARE VARIOUS TYPES OF BUSINESS OWNERSHIP? DIFFERENTIATE BETWEEN PUBLIC AND PRIVATE COMPANY. DEFINE A JOINT STOCK COMPANY, ITS CHARACTERISTICS AND INCORPORATION PROCEDURE.

8) WHAT ROLE THE STOCK EXCHANGE PLAYS IN THE ECONOMY OF A COUNTRY.

9) DEFINE INSURANCE, WHAT ARE VARIOUS TYPES OF INSURANCE? LIST AND EXPLAIN BUSINESS RISK.IMPORTANCE OF INSURANCE. CHARACTERISTICS OF INSURABLE RISK.

A) QUALITIES OF A GOOD BUSINESS MAN

B) INVENTORY CONTROL

C) BUSINESS COMBINATIONS

D) WAGE INCENTIVE PLANS

E) TRANSPORTATION

F) SELECTION PROCEDURE OF STAFF

G) SALES PROMOTION

H) SERVICES OF A WHOLE SELLER

I) MARKETING (DEFINITION AND IMPORTANCE)

J) ADVERTISING

Thursday, December 26, 2013

B.COM PART 1 2013 EXAMS , STATISTICS AND BUSINESS MATHS, PLEASE PREPARE LAST 5 YEAR'S REGULAR AND PRIVATE QUESTIONS.

B.COM PART 1 , STATISTICS AND BUSINESS MATHS, PLEASE PREPARE LAST 5 YEAR'S REGULAR AND PRIVATE QUESTIONS.

Saturday, December 21, 2013

B.COM PART 2 : BANKING IMPORTANT QUESTIONS 2013

B.COM PART 2 : BANKING IMPORTANT QUESTIONS 2014

BANKING & FINANCE – IMPORTANT QUESTIONS

BY KHALID AZIZ

1) Define a bank and explain its evolution. Describe various functions of a commercial bank.

2) Define a central bank, list its functions and explain them.

3) Define credit instruments and briefly describe their kinds.

4) Define a cheque and describe briefly its kinds and why a cheque is dishonored by bank.

5) Write note on State Bank of Pakistan. What are relations between scheduled banks and SBP?

6) State the kinds of bank account and list the steps involved in opening a bank account.

7) Define endorsement and describe its kinds.

8) Describe in detail the principles of employing bank fund.

9) How does a bank create credit?

10) What is working capital? What are its functions and importance? What is equation of working

capital?

11) What is business finance and describe its types.

12) Short Notes

a) Credit control

b) Bill of exchange

c) Promissory Note

d) Discounting a bill of exchange

e) Letter of credit

f) Noting and protesting

g) Qarz e Hasana

h) Distinguish between qarz e hasana and loan

i) Modarba & Musharka

j) NIT

k) IDBP

l) Islamic Banking

m) Interest free banking

n) Markup and interest

o) Sources of business finance

BANKING & FINANCE – IMPORTANT QUESTIONS

BY KHALID AZIZ

1) Define a bank and explain its evolution. Describe various functions of a commercial bank.

2) Define a central bank, list its functions and explain them.

3) Define credit instruments and briefly describe their kinds.

4) Define a cheque and describe briefly its kinds and why a cheque is dishonored by bank.

5) Write note on State Bank of Pakistan. What are relations between scheduled banks and SBP?

6) State the kinds of bank account and list the steps involved in opening a bank account.

7) Define endorsement and describe its kinds.

8) Describe in detail the principles of employing bank fund.

9) How does a bank create credit?

10) What is working capital? What are its functions and importance? What is equation of working

capital?

11) What is business finance and describe its types.

12) Short Notes

a) Credit control

b) Bill of exchange

c) Promissory Note

d) Discounting a bill of exchange

e) Letter of credit

f) Noting and protesting

g) Qarz e Hasana

h) Distinguish between qarz e hasana and loan

i) Modarba & Musharka

j) NIT

k) IDBP

l) Islamic Banking

m) Interest free banking

n) Markup and interest

o) Sources of business finance

Thursday, December 19, 2013

B.COM PART 2: AUDITING AND INCOME TAX , IMPORTANT QUESTION 2013

B.COM PART 2: AUDITING AND INCOME TAX , IMPORTANT QUESTION 2013.

AUDITING – IMPORTANT QUESTIONS

BY KHALID AZIZ

1) Define auditing and describe its objectives.

2) Define investigation and distinguish it with auditing.

3) Describe the rights and duties of an auditor.

4) What are various types of audit?

5) What are audit work papers? What are their purposes? What are the usual contents

of audit work papers?

6) Define audit techniques, name them and explain any five of them.

7) What is meant by evidence in auditing? Name the various types of audit evidence.

8) Write a detailed note on audit program.

9) Distinguish between financial audit and cost audit.

10)What points should be considered while auditing the annual accounts of a hotel &

restaurant, Banks, Doctors, Educational institutions, charitable institutions.

11)What are divisible profits? What should be the guiding principles in determining the

divisible profits?

12) Explain the importance of an accurate valuation of inventories and list steps for the

verification of inventories.

13)Define fraud and explain types of fraud.

14)Write detailed notes on internal control, internal audit and cost audit.

15)Audit report (qualified and unqualified)

16) Income tax short notes:

A. Total income

B. Income year

C. Sales tax

D. Income tax authorities

E. Powers of income tax officers

F. Tax payers

G. Central board of revenue (cbr)

H. Registered firm

I. Persons

J. Assessment year

K. Appellate tribunal

L. Assessee

M. Casual income

N. Self assessment scheme

AUDITING – IMPORTANT QUESTIONS

BY KHALID AZIZ

1) Define auditing and describe its objectives.

2) Define investigation and distinguish it with auditing.

3) Describe the rights and duties of an auditor.

4) What are various types of audit?

5) What are audit work papers? What are their purposes? What are the usual contents

of audit work papers?

6) Define audit techniques, name them and explain any five of them.

7) What is meant by evidence in auditing? Name the various types of audit evidence.

8) Write a detailed note on audit program.

9) Distinguish between financial audit and cost audit.

10)What points should be considered while auditing the annual accounts of a hotel &

restaurant, Banks, Doctors, Educational institutions, charitable institutions.

11)What are divisible profits? What should be the guiding principles in determining the

divisible profits?

12) Explain the importance of an accurate valuation of inventories and list steps for the

verification of inventories.

13)Define fraud and explain types of fraud.

14)Write detailed notes on internal control, internal audit and cost audit.

15)Audit report (qualified and unqualified)

16) Income tax short notes:

A. Total income

B. Income year

C. Sales tax

D. Income tax authorities

E. Powers of income tax officers

F. Tax payers

G. Central board of revenue (cbr)

H. Registered firm

I. Persons

J. Assessment year

K. Appellate tribunal

L. Assessee

M. Casual income

N. Self assessment scheme

Wednesday, December 18, 2013

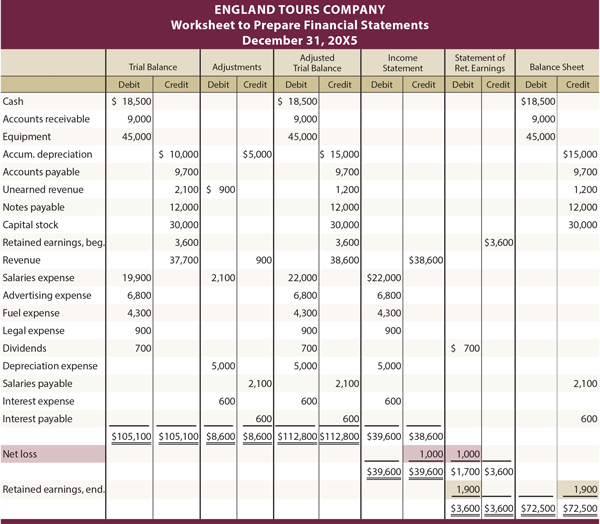

Steps in Preparing the Worksheet:

Steps in Preparing the Worksheet:

| In smaller companies the adjustments are usually entered directly in the journal and posted to the ledger, and the financial statements are prepared directly from the adjusted trial balance. For larger companies, however, which may require many adjusting entries, a worksheet is essential. The work sheet is identified by a heading that consists of the name of the company, the title "Work Sheet", and the period of time covered (as on the income statement). There are five steps in the preparation of a work sheet, as shown below: (i) Entering the Account Balances in the Trial Balance Column: The titles and balances of the accounts are copied directly from the ledger into the trial balance columns. When a work sheet is prepared, a separate trial balance in not required. However, if it has been prepared, the balances may be posted from it in the work sheet. (ii) Entering the Adjustments in the Adjustment Columns: Adjustments have been already explained. The same adjustments are entered in the adjustment columns of the work sheet as shown in earlier example. As each adjustment is entered, a letter is used to identify the debit and credit parts of the same entry. In practice, this letter may be used to reference supporting computations or documentation underlying the adjusting entry. When all the adjustments have been entered in relevant debit and credit columns, the pair of adjustments columns must be added. This step proves that the debits and credits of the adjustments are equal and generally reduces error in the preparation of the work sheet. (iii) Entering the Account Balances as Adjusted in the Adjusted Trial Balance Columns: The adjusted trial balance prepared by combining the amount of each account in the original trial balance columns with the corresponding amounts in the adjustment's columns and entering the combined amounts on a line by line basis in the adjusted trial balance columns. Adjusted trial balance columns are then footed, that is totaled, to check the arithmetical accuracy of tile cross footing just like that of a normal trial balance. Some accountants prefer to eliminate the adjusted trial balance columns and to extend the adjusted account balances directly to the appropriate statement column for 7 to 12. Such an alternative form of work sheet is especially popular if there are only a few items involved, it would then be called a "Jen Column Work Sheet". (iv) Extending the Account Balance from the Adjusted Trial Balance Column to the Profit & Loss Columns or the Balance Sheet Columns, (i.e. from column 5 and 6 to column 7 to 12): Every account in the adjusted trial balance is either a balance sheet account or an income statement account. The accounts are sorted, and each account is extended to its proper place as a debit or credit either in the balance sheet columns or in the trading and profit & loss columns. The result of extending the accounts is shown in example-(A). Revenue (profits) and expenses accounts are moved to the profit & loss columns. Assets and liabilities as welt as capital and drawings accounts are then extended to the balance sheet columns. To avoid over looking an account, extend the accounts line by line, beginning with the first line (which is cash) and not omitting any. (v) Totaling the Income Statement Columns and the Balance Sheet Columns. Enter the Net Income or Net Loss in Both Pairs of Columns as a Balancing Figure, and Re-compute Column Totals: This last step as shown in example-(A) is necessary to compute net income or net loss and to prove the arithmetical accuracy of the work sheet. Net income or net loss is equal to the difference between the debit and credit columns of the income statement. In the illustrative example-(A), the revenue has exceeded the expenses. Consequently, the company has a net profit of $45,030. This amount of $45,030 is entered in the debit side of the income statement (PLS A/C) columns to balance the columns and it is entered on the credit side of the balance sheet columns. This is done because excess revenue (net income) increases capital and increases in owner's capital are recorded by credits. If a net loss had occurred, the opposite rule world apply. Example and its Solution for the Preparation of Worksheet:Example-(A):

X & Y Company

The trial balance of X & Y Company, as on 30th June is given below:

Following additional information is also available: (i) Closing stock on 30th June is $45,000 (ii) Charge depreciation at 10% on (a) Plant and machinery (b) Furniture. (iii) Make provision for bad and doubtful debts at 5% of sundry debtors. (iv) $150 on account of insurance are prepaid. Required: Prepare: (a) Trading and P & L Account. (b) Balance sheet as on 30th June. Solution:

X & Y Company

Trading, Profit & Loss Account

For the year ended 30th June

X & Y Company

Balance Sheet as on 30th June

Example-(B): This solved problem illustrates the use of a work sheet where the columns of trading and profit & loss account has been substituted by Income Statement column . The trial balance for the B & M Delivery Company as on December 31, was as follows:

B & M Delivery Company

(a) Insurance expense for the month of December $200 (b) Rent expense for the month of December $400 (c) Supplies used during the month $500 (d) Depreciation for December $50 (e) One-third of the fees-received in advance account has been earned by 31st December. (f) Interest earned but not yet received $600 (g) Unbilled service $1000 (h) Accrued salaries $180

B & M Delivery Company Worksheet as on 31st December

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Tuesday, December 17, 2013

KARACHI UNIVERSITY NAY B.COM REGULAR 2013 KA SCHEDULE ANNOUNCE KARDIA HAY.

KARACHI UNIVERSITY NAY B.COM

REGULAR 2013 KA SCHEDULE

ANNOUNCE KARDIA HAY.

REGULAR 2013 KA SCHEDULE

ANNOUNCE KARDIA HAY.

Subscribe to:

Posts (Atom)

B.COM COACHING AND HOME TUITION