Tuesday, December 27, 2011

Sunday, December 18, 2011

Saturday, December 17, 2011

Wednesday, December 14, 2011

Sunday, December 11, 2011

UN-OFFICIAL DATE SHEET B.COM KARACHI UNIVERSITY EXAMS 2011

Wednesday, November 30, 2011

Monday, November 28, 2011

Motivation in theory - Herzberg two factor theory

Herzberg's Two Factor Theory is a "content theory" of motivation" (the other main one is Maslow's Hierarchy of Needs).

Herzberg analysed the job attitudes of 200 accountants and engineers who were asked to recall when they had felt positive or negative at work and the reasons why.

From this research, Herzberg suggested a two-step approach to understanding employee motivation and satisfaction:

Hygiene Factors

Hygiene factors are based on the need to for a business to avoid unpleasantness at work. If these factors are considered inadequate by employees, then they can cause dissatisfaction with work. Hygiene factors include:

- Company policy and administration

- Wages, salaries and other financial remuneration

- Quality of supervision

- Quality of inter-personal relations

- Working conditions

- Feelings of job security

Motivator Factors

Motivator factors are based on an individual's need for personal growth. When they exist, motivator factors actively create job satisfaction. If they are effective, then they can motivate an individual to achieve above-average performance and effort. Motivator factors include:

- Status

- Opportunity for advancement

- Gaining recognition

- Responsibility

- Challenging / stimulating work

- Sense of personal achievement & personal growth in a job

There is some similarity between Herzberg's and Maslow's models. They both suggest that needs have to be satisfied for the employee to be motivated. However, Herzberg argues that only the higher levels of the Maslow Hierarchy (e.g. self-actualisation, esteem needs) act as a motivator. The remaining needs can only cause dissatisfaction if not addressed.

Applying Hertzberg's model to de-motivated workers

What might the evidence of de-motivated employees be in a business?

- Low productivity

- Poor production or service quality

- Strikes / industrial disputes / breakdowns in employee communication and relationships

- Complaints about pay and working conditions

According to Herzberg, management should focus on rearranging work so that motivator factors can take effect. He suggested three ways in which this could be done:

Hygiene Factors

Hygiene factors are based on the need to for a business to avoid unpleasantness at work. If these factors are considered inadequate by employees, then they can cause dissatisfaction with work. Hygiene factors include:

- Company policy and administration

- Wages, salaries and other financial remuneration

- Quality of supervision

- Quality of inter-personal relations

- Working conditions

- Feelings of job security

Motivator Factors

Motivator factors are based on an individual's need for personal growth. When they exist, motivator factors actively create job satisfaction. If they are effective, then they can motivate an individual to achieve above-average performance and effort. Motivator factors include:

- Status

- Opportunity for advancement

- Gaining recognition

- Responsibility

- Challenging / stimulating work

- Sense of personal achievement & personal growth in a job

There is some similarity between Herzberg's and Maslow's models. They both suggest that needs have to be satisfied for the employee to be motivated. However, Herzberg argues that only the higher levels of the Maslow Hierarchy (e.g. self-actualisation, esteem needs) act as a motivator. The remaining needs can only cause dissatisfaction if not addressed.

Applying Hertzberg's model to de-motivated workers

What might the evidence of de-motivated employees be in a business?

- Low productivity

- Poor production or service quality

- Strikes / industrial disputes / breakdowns in employee communication and relationships

- Complaints about pay and working conditions

According to Herzberg, management should focus on rearranging work so that motivator factors can take effect. He suggested three ways in which this could be done:

Tuesday, November 22, 2011

Saturday, November 19, 2011

Wednesday, November 16, 2011

Tuesday, November 15, 2011

Friday, November 11, 2011

Agriculture Problems in Pakistan And Their Solutions

Economy of every state depends on three sectors i.e agriculture, industry and commerce. These three are interrelated with each other as the progress or retrogress of one sector effects the other two. Pakistan is an agricultural state thus agriculture gains are of much importance than any other sector. Importance of this sector is manifold as it feeds people, provides raw material for industry and is a base for foreign trade. Foreign exchange earned from merchandise exports is 45% of total exports of Pakistan. It contributes 26% of GDP and 52% of the total populace is getting its livelihood from it. 67.5% people are living in the rural areas of Pakistan and are directly involved in it.

There are two crops in Pakistan ie Rabi & Kharif. Crop | Sowing season | Harvesting season Kharif | April – June | Oct – Dec Rabi | Oct – Dec | April – May Major crops of Pakistan are wheat, rice, maize, cotton and sugar cane. These major crops contributed 7.7% last year against the set target of 4.5%. Minor crops are canola, onions, mangoes and pulses which contributed 3.6% as there was no virus attack last year. Fishery and Forestry contributes 16.6% and 8.8% respectively. Though the agricultural sector is facing problems in Pakistan yet the major chunk of money comes from this sector. Following are the major causes of agricultural problems in Pakistan which disturb the agricultural growth or development in Pakistan.

Firstly,No mechanism has been adopted to eradicate the soil erosion and even after harvesting nothing is done to improve or restore the soil energy. Therefore, the fertility of soil is decreasing day by day. The thickness of fertile layer of soil in Pakistan is more than 6 inches but the average yield is lower than other countries where layer of fertile soil is only 4 inches.

Secondly, water wastage is very high in our country. The archaic method of flood irrigation is still in practice in whole of the country which wastes almost 50 to 60 percent of water. A new irrigation system called drip irrigation system has been introduced in many parts of the world. This not only saves water but also gives proper quantity of water according to the needs of plants.

Thirdly, owing old methods of cultivation and harvesting, Pakistan has low yield per acre that means the average crop in Pakistan is just 1/4th of that of advance states. Where as Nepal, India and Bangladesh are using modern scientific methods to increase their yield per acre. For this purpose, these states are using modern machines to improve their yield.

Fourthly, the small farmers are increasing in our country as the lands are dividing generation by generation. So, there are large number of farmers who own only 4 acres of land. These small farmers do not get credit facilities to purchase seeds, pesticides, fertilizers etc. Additionally, a large area of land is owned by feudals and the farmers who work on their lands, are just tenants. This uncertain situation of occupancy neither creates incentive of work nor does attract capital investment.

Fifthly,water logging and salinity is increasing day by day. No effective measures have been taken to curb it. As the storage capacity of the dams is decreasing so the water availability per acre is also decreasing. Therefore, the farmers are installing more and more tube wells to irrigate their crops. This is why salinity is becoming the major issue in most parts of Punjab and Sindh.

Sixthly,focusing more on land, crops and yield problems the man behind the plough is always ignored. While formulating the 5 or 10 years plan, no emphasize has been laid on the importance of solving the problems of farmers. Most of the farmers are illiterate, poor and ignorant. In this wake the loans issued by ADBP or other banks are used by them in other fields like repayment of debts, marriage of daughters etc, in spite of its befitting use in agricultural sector.

Lastly, The only mean of communication in rural areas is T.V or radio so it is urgently needed on the part of these mass communication resources to air the programmes related to the new agricultural techniques and allied sciences. But these programmes should be telecast in regional or local languages. Because lack of guidance is the main reason of farmers backwardness. The communication gap between well qualified experts and simple farmers have not been bridged. Availability of these experts is not ensured in rural areas as they are reluctant to go there.

Solutions For Agricultural Problems

In Pakistan: Feudalism should be abolished and lands should be allotted to poor farmers. This will enhance the productivity and per acre yield of all the crops in Pakistan. Taxes should be levied on Agricultural income but not without devising limit of land holding. Other wise it would directly effect poor farmers. Federal Seed Certification and Federal Seed Registration is approved but it should taken responsible steps in approving seeds as it has already approved 36 new kinds of seeds. Specially, those seeds should be banned which can create pest problem in near future. These seeds are of cotton mainly. International seed makers are providing those seeds which are not successful in our country as these seeds are not tested on our soil. A new Agricultural policy must be framed in which following steps should be focussed on. - Small farmer must be focused. The major problems of small farmers should be solved first. - Consumer friendly policy must be projected. - Productivity enhancement programme must be constituted to adjust and support prices. - Different Agricultural zones should be introduced. As Multan in famous for its Mangoes and citrus fruits so it must be made Mango, citrus zone by which Perishable products should be exported. This would enhance agro based industry and increase foreign reserves. Pakistan Agricultural storage & Services Corporation needs to take steps in this regard. - Corporate farming like giving lands to Mitehels, Nestle and Multinational companies is also a good idea that will also help those who own a large area of fertile land but can’t manage it. - Surplus vegetables and fruits must be exported. A Rs 39 million scheme has been approved for the current fiscal year for establishment of agro export processing zone for fruits, vegetables and flowers. This will also help in commercializing agriculture - Latest mechinery should be provided to the farmers to increase the per acre yield. This provision should be on easy installments so that the farmers can avoid the burden of loans. If possible subsidy should be given by the government of modern machinery.- Modern techniques of irrigation can solve the problems of irrigation in Pakistan. This includes drip irrigation and sprinkle irrigation methods. By using this technique the farmers can save a huge some of money which he pays for irrigation through tubewells and tracktors. - More dams should be constructed on Indus, Jehlum and Chenab rivers. This will enhance the storage capacity of water and reduce the per acre cost of all the crops. This step will also reduce the salinity chances of the lands as less tubewell water will be flooded to the lands which cause salinity.

There are two crops in Pakistan ie Rabi & Kharif. Crop | Sowing season | Harvesting season Kharif | April – June | Oct – Dec Rabi | Oct – Dec | April – May Major crops of Pakistan are wheat, rice, maize, cotton and sugar cane. These major crops contributed 7.7% last year against the set target of 4.5%. Minor crops are canola, onions, mangoes and pulses which contributed 3.6% as there was no virus attack last year. Fishery and Forestry contributes 16.6% and 8.8% respectively. Though the agricultural sector is facing problems in Pakistan yet the major chunk of money comes from this sector. Following are the major causes of agricultural problems in Pakistan which disturb the agricultural growth or development in Pakistan.

Firstly,No mechanism has been adopted to eradicate the soil erosion and even after harvesting nothing is done to improve or restore the soil energy. Therefore, the fertility of soil is decreasing day by day. The thickness of fertile layer of soil in Pakistan is more than 6 inches but the average yield is lower than other countries where layer of fertile soil is only 4 inches.

Secondly, water wastage is very high in our country. The archaic method of flood irrigation is still in practice in whole of the country which wastes almost 50 to 60 percent of water. A new irrigation system called drip irrigation system has been introduced in many parts of the world. This not only saves water but also gives proper quantity of water according to the needs of plants.

Thirdly, owing old methods of cultivation and harvesting, Pakistan has low yield per acre that means the average crop in Pakistan is just 1/4th of that of advance states. Where as Nepal, India and Bangladesh are using modern scientific methods to increase their yield per acre. For this purpose, these states are using modern machines to improve their yield.

Fourthly, the small farmers are increasing in our country as the lands are dividing generation by generation. So, there are large number of farmers who own only 4 acres of land. These small farmers do not get credit facilities to purchase seeds, pesticides, fertilizers etc. Additionally, a large area of land is owned by feudals and the farmers who work on their lands, are just tenants. This uncertain situation of occupancy neither creates incentive of work nor does attract capital investment.

Fifthly,water logging and salinity is increasing day by day. No effective measures have been taken to curb it. As the storage capacity of the dams is decreasing so the water availability per acre is also decreasing. Therefore, the farmers are installing more and more tube wells to irrigate their crops. This is why salinity is becoming the major issue in most parts of Punjab and Sindh.

Sixthly,focusing more on land, crops and yield problems the man behind the plough is always ignored. While formulating the 5 or 10 years plan, no emphasize has been laid on the importance of solving the problems of farmers. Most of the farmers are illiterate, poor and ignorant. In this wake the loans issued by ADBP or other banks are used by them in other fields like repayment of debts, marriage of daughters etc, in spite of its befitting use in agricultural sector.

Lastly, The only mean of communication in rural areas is T.V or radio so it is urgently needed on the part of these mass communication resources to air the programmes related to the new agricultural techniques and allied sciences. But these programmes should be telecast in regional or local languages. Because lack of guidance is the main reason of farmers backwardness. The communication gap between well qualified experts and simple farmers have not been bridged. Availability of these experts is not ensured in rural areas as they are reluctant to go there.

Solutions For Agricultural Problems

In Pakistan: Feudalism should be abolished and lands should be allotted to poor farmers. This will enhance the productivity and per acre yield of all the crops in Pakistan. Taxes should be levied on Agricultural income but not without devising limit of land holding. Other wise it would directly effect poor farmers. Federal Seed Certification and Federal Seed Registration is approved but it should taken responsible steps in approving seeds as it has already approved 36 new kinds of seeds. Specially, those seeds should be banned which can create pest problem in near future. These seeds are of cotton mainly. International seed makers are providing those seeds which are not successful in our country as these seeds are not tested on our soil. A new Agricultural policy must be framed in which following steps should be focussed on. - Small farmer must be focused. The major problems of small farmers should be solved first. - Consumer friendly policy must be projected. - Productivity enhancement programme must be constituted to adjust and support prices. - Different Agricultural zones should be introduced. As Multan in famous for its Mangoes and citrus fruits so it must be made Mango, citrus zone by which Perishable products should be exported. This would enhance agro based industry and increase foreign reserves. Pakistan Agricultural storage & Services Corporation needs to take steps in this regard. - Corporate farming like giving lands to Mitehels, Nestle and Multinational companies is also a good idea that will also help those who own a large area of fertile land but can’t manage it. - Surplus vegetables and fruits must be exported. A Rs 39 million scheme has been approved for the current fiscal year for establishment of agro export processing zone for fruits, vegetables and flowers. This will also help in commercializing agriculture - Latest mechinery should be provided to the farmers to increase the per acre yield. This provision should be on easy installments so that the farmers can avoid the burden of loans. If possible subsidy should be given by the government of modern machinery.- Modern techniques of irrigation can solve the problems of irrigation in Pakistan. This includes drip irrigation and sprinkle irrigation methods. By using this technique the farmers can save a huge some of money which he pays for irrigation through tubewells and tracktors. - More dams should be constructed on Indus, Jehlum and Chenab rivers. This will enhance the storage capacity of water and reduce the per acre cost of all the crops. This step will also reduce the salinity chances of the lands as less tubewell water will be flooded to the lands which cause salinity.

Wednesday, October 26, 2011

NEW REGISTRATION DATES FOR B.COM EXTERNAL EXAMS 2011

NEW REGISTRATION DATES FOR B.COM EXTERNAL EXAMS 2011

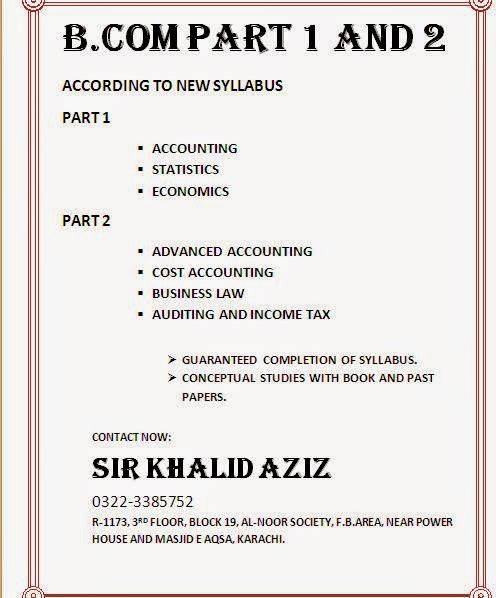

CRASH CLASSES B.COM 1 & 2

ACCOUNTING, STATISTICS, ECONOMICS AND ADVANCED & COST ACCOUNTING IN JUST 30 CLASSES.

CRASH CLASSES B.COM 1 & 2

ACCOUNTING, STATISTICS, ECONOMICS AND ADVANCED & COST ACCOUNTING IN JUST 30 CLASSES.

Tuesday, October 18, 2011

Sunday, October 16, 2011

Wednesday, October 12, 2011

Tuesday, October 11, 2011

CRASH CLASSES B.COM 1 & 2

CRASH CLASSES B.COM 1 & 2

IN ONLY 30 DAYS

ALL IMPORTANT SUBJECTS.

CONTACT NOW

KHALID AZIZ

0322-3385752

IN ONLY 30 DAYS

ALL IMPORTANT SUBJECTS.

CONTACT NOW

KHALID AZIZ

0322-3385752

Friday, October 7, 2011

Sunday, October 2, 2011

GUESS PAPERS AVAILABLE FOR B.COM & B.A

GUESS PAPERS AVAILABLE FOR B.COM & B.A

KHALID AZIZ

0322-3385752

KARACHI.

KHALID AZIZ

0322-3385752

KARACHI.

Tuesday, September 27, 2011

Wednesday, September 7, 2011

BUSINESS LAW: PROVISIONS REGARDING HEALTH & SAFETY

Health and Safety

13. Cleanliness. -

(1) Every factory shall be kept clean and free from effluvia arising from any drain, privy or other nuisance, and in particular, -

(a) accumulation of dirt and refuse shall be removed daily by sweeping or by any other effective method from the floors and benches of work-rooms and from staircases and disposed of in a suitable manner ;

(b) the floor of every work-room shall be cleaned at least once in every week by washing, using disinfectant where necessary or by some other effective method ;

(c) where the floor is liable to become wet in the course of any manufacturing process to such extent as is capable of being drained, effective means of drainage shall be provided and maintained ;

(d) all inside walls and partitions, all ceilings, or tops of rooms and walls, sides and tops or passages and staircases shall -

(i) where they are painted or varnished, be repainted or revarnished at least once in every five years ;

(ii) where they arc painted or varnished and have smooth impervious surfaces, be cleaned at least once in every fourteen months, by such methods as may be prescribed ;

(iii) in any other case, kept whitewashed or colour washed and the whitewashing or colour washing shall be carried out at least once in every fourteen months ; and

(e) the dates on which the processes required by clause (d) are carried out shall be entered in the prescribed register.

(2) If, in view of the nature of the operations carried on in a factory it is not possible for the occupier to comply with all or any of the provisions of sub-section (1), the Provincial Government may, by an order, exempt such factory or class or description of factories from any of the provisions of that sub-section and specify alternative methods for keeping the factory in a clean state.

14. Disposal of wastes and effluents. -

(1) Effective arrangements shall be made in every factory for the disposal of wastes and effluents due to the manufacturing process carried on therein.

(2) The Provincial Government may make rules prescribing the arrangements to be made under sub-section (1) or requiring that the arrangements made in accordance with that sub-section shall be subject to the approval of such authority as may be prescribed.

15. Ventilation and temperature. -

(1) Effective and suitable provisions shall be made in every factory for securing and maintaining in every work-room -

(a) adequate ventilation by the circulation of fresh air, and

(b) such temperature as will secure to workers therein reasonable conditions of comfort and prevent injury to health, and in particular -

(i) the walls and roofs shall be of such material and so designed that such temperature shall not be exceeded but kept as low as practicable ;

(ii) where the nature of the work carried on in the factory involves, or is likely to involve, the production of excessively high temperature, such adequate measures as are practicable shall be taken to protect the workers therefrom by separating the process which produces such temperature from the work-room by insulating the hot parts or by other effective means.

(2) The Provincial Government may prescribe a standard of adequate ventilation and reasonable temperature for any factory or class or description of factories or parts thereof and direct that a thermometer shall be provided and maintained in such place and position as may be specified.

(3) If it appears to the Provincial Government that in any factory or class or description of factories excessively high temperature can be reduced by such methods as whitewashing, spraying or insulating and screening outside walls or roofs or windows, or by raising the level of the roof, or by insulating the roof either by an air space and double roof or by the use of insulating roof materials, or by other methods, it may prescribe such of these or other methods to be adopted in the factory.

16. Dust and fume. -

(1) In every factory in which, by reason of the manufacturing process carried on, there is given off any dust or fume or other impurity of such a nature and to such an extent as is likely to be injurious or offensive to the workers employed therein, effective measures shall be taken to prevent its accumulation in any work-room and its inhalation by workers and if any exhaust appliance is necessary for this purpose, it shall be applied as near as possible to the point of origin of the dust, fume or other impurity, and such point shall be enclosed so far as possible.

(2) In any factory no stationary internal combustion engine shall be operated unless the exhaust is conducted into open air and exhaust pipes are insulated to prevent scalding and radiation heat, and no internal combustion engine shall be operated in any room unless effective measures have been taken to prevent such accumulation of fumes therefrom as are likely to be injurious to the workers employed in the work-room.

17. Artificial humidification. -

(1) The Provincial Government may, in respect of all factories in which humidity of the air is artificially increased, make rules -

(a) prescribing standards of humidification ;

(b) regulating the methods used for artificially increasing the humidity of the air ;

(c) directing prescribed tests for determining the humidity of the air to be correctly carried out and recorded, and

(d) prescribing methods to be adopted for securing adequate ventilation and cooling of the air in the work-rooms.

(2) In any factory in which the humidity of the air is artificially increased, the water used for the purpose shall be taken from a public supply, or other source of drinking water, or shall be effectively purified before it is so used.

(3) If it appears to an Inspector that the water used in a factory for increasing humidity which is required to be effectively purified under sub-section (2) is not effectively purified, he may serve on the Manager of the factory an order in writing specifying the measures which, in his opinion, should be adopted, and requiring them to be carried out before a specified date.

18. Overcrowding. -

(1) No work-room in any factory shall be over-crowded to an extent injurious to the health of the workers employed therein.

(2) Without prejudice to the generality of the provisions of sub-section (1) there shall be provided for every worker employed in a work-room -

(a) at least three hundred and fifty cubic feet of space in the case of a factory in existence on the date of the commencement1 of the Labour Laws (Amendment) Ordinance, 1972; and

(b) at least five hundred cubic feet of space in the case of a factory built after the commencement of the Labour Laws (Amendment) Ordinance, 1972.

Explanation. - For the purpose of this sub-section no account shall be taken of a space which is more than fourteen feet above the level of the floor of the room.

(3) If the Chief Inspector by order in writing so requires, there shall be posted in each work-room of a factory a notice specifying the maximum number of workers who may in compliance with the provisions of this section be employed in the room.

(4) The Chief Inspector may, by order in writing, exempt, subject to such conditions as he may think fit to impose, any work-room from the provisions of this section if he is satisfied that compliance therewith in respect of such room is not necessary for the purpose of health of the workers employed therein.

19. Lighting. -

(1) In every part of a factory where workers are working or passing, there shall be provided and maintained -

(a) sufficient and suitable lighting, natural or artificial, or both; and

(b) emergency lighting of special points in work-room and passages to function automatically in case of a failure of the ordinary electric system.

(2) In every factory all glazed windows and sky-lights used for the lighting of the work-room shall be kept clean on both the outer and inner surfaces and free from obstruction as far as possible under the rules framed under sub-section (3) of section 15.

(3) In every factory effective provisions shall, so far as is practicable, be made for the prevention of -

(a) glare either directly from any source of light or by reflection from a smooth or polished surface; and

(b) the formation of shadows to such an extent as to cause eye strain or risk of accident to any worker.

(4) The Provincial Government may prescribe standards of sufficient and suitable lighting for factories or for any class or description of factories or for any manufacturing process.

20. Drinking Water. -

(1) In every factory effective arrangements shall be made to provide and maintain at suitable points conveniently situated for all workers employed therein a sufficient supply of whole-some drinking water.

(2) All such points shall be legibly marked "Drinking Water" in a language understood by the majority of the workers and no such point shall be situated within twenty feet of any washing place, urinal or latrine, unless a shorter distance is approved in writing by the Chief Inspector.

(3) In every factory wherein more than two hundred and fifty workers are ordinarily employed, provision shall be made for cooling the drinking water during the hot weather by effective means and for distribution thereof and arrangements shall also be made for -

(a) the daily renewal of water if not laid on; and

(b) a sufficient number of cups or other drinking vessels, unless the water is being delivered in an upward jet.

(4) The Provincial Government may, in respect of all factories or any class or description of factories, make rules for securing compliance with the provisions of this section.

21. Latrines and urinals. -

(1) In every factory -

(a) sufficient latrines and urinals of prescribed types shall be provided conveniently situated and accessible to workers at all times while they are in the factory;

(b) enclosed latrines and urinals shall be provided separately for male and female workers;

(c) such latrines and urinals shall be adequately lighted and ventilated and no latrine and urinal shall, unless specially exempted in writing by the Chief Inspector, communicate with any workroom except through an intervening open space or ventilated passage;

(d) all such latrines and urinals shall be maintained in a clean and sanitary condition at all times with suitable detergents or disinfectants or with both;

(e) the floors and internal walls of the latrines and urinals and the sanitary blocks shall, up to a height of three feet, be finished to provide a smooth polished impervious surface; and

(f) washing facilities shall be provided near every sanitary convenience.

(2) The Provincial Government may prescribe the number of latrines and urinals to be provided in any factory in proportion to the number of male and female workers ordinarily employed therein and such further matters in respect of sanitation in the factories as it may deem fit.

22. Spittoons. -

(1) In every factory there shall be provided, at convenient places, a sufficient number of spittoons which shall be maintained in a clean and hygienic condition.

(2) The Provincial Government may make rules prescribing the type and the number of spittoons to be provided and their location in any factory and such further matters as may be deemed necessary relating to their maintenance in a clean and hygienic condition.

(3) No person shall spit within the premises of a factory except in the spittoons provided for the purpose. A Notice containing this provision and the penalty for its violation shall be prominently displayed at suitable places in the premises.

(4) Whosoever spits in contravention of sub-section (3) shall be punishable with a fine not exceeding two rupees.

23. Precautions against contagious or infections disease. -

(1) Each worker in a factory shall be provided with a "Hygiene Card' in which during the month of January and July every year entries shall be recorded after examination by appointed factory doctor to the effect that the worker is not suffering from any contagious or infectious disease. The fee of such an examination shall be fixed by the Provincial Government and will be borne by the occupier or manager of the factory.

(2) If a worker is found to be suffering from any contagious or infectious disease on an examination under sub-section (1), he shall not be appointed on work till he is declared free of such a disease.

23-A. Compulsory vaccination and inoculation. - Each worker in a factory shall be vaccinated and inoculated against such diseases and at such intervals as may be prescribed. The expenses, if any, of such vaccination and inoculation shall be borne by the occupier or manager of the factory.

24. Power to make rules for provision of canteens. -

(1) The Provincial Government may make rules requiring that in any specified factory wherein more than two hundred and fifty workers are ordinarily employed, an adequate canteen shall be provided for the use of the workers.

(2) Without prejudice to the generality of the foregoing power, such rules may provide for -

(a) the date by which such canteen shall be provided;

(b) the standards in respect of construction, accommodation, furniture and other equipment of the canteen;

(c) the foodstuffs to be served therein and the charges which may be made therefor;

(d) representation of the workmen in the management of the canteens;

(e) enabling, subject to such conditions, if any, as may be specified, the power to make rules under clause (c) to be exercised also by the Chief Inspector.

24-A. Welfare Officer. - In every factory wherein not less than five hundred workers are ordinarily employed the occupier or manager shall employ such number of welfare officers, having such qualifications, to perform such duties and on such terms and conditions as may be prescribed.

25. Precautions in case of fire. -

(1) Every factory shall be provided with such means of escape in case of fire as may be prescribed.

(2) If it appears to the Inspector that any factory is not provided with the means of escape prescribed under sub-section (1) he may serve on the manager of the factory an order in writing specifying the measures which should be adopted before a date specified in the order.

(3) In every factory the doors affording exit from any room shall not be locked or fastened so that they can be easily and immediately opened from inside while any person is within the room, and all such doors, unless they are of the sliding type, shall be constructed to open outwards or where the door is between two rooms, in the direction of the nearest exit from the building and such door shall not be locked or obstructed while work is being carried on in the room and shall at all times be kept free from any obstruction.

(4) In every factory every window, door or other exit affording means of escape in case of fire, other than means of exit in ordinary use, shall be distinctively marked in a language understood by the majority of the workers and in red letters of adequate size or by some other effective and clearly understood sign.

(5) In every factory there shall be provided effective and clearly audible means of giving warning in case of fire to every person employed therein.

(6) A free passage-way giving access to each means of escape in case of fire shall be maintained for the use of all workers in every room of the factory.

(7) In every factory wherein more than ten workers are ordinarily employed in any place above the ground floor, or explosive or highly inflammable materials are used or stored, effective measures shall be taken to ensure that all the workers are familiar with the means of escape in case of fire and have been adequately trained in the routine to be followed in such case.

(8) The Provincial Government may make rules prescribing in respect of any factory, or class or description of factories, the means of escape to be provided in case of fire and the nature and amount of firefighting apparatus to be provided and maintained.

26. Fencing of machinery. -

(1) In every factory the following shall be securely fenced by the safeguards of substantial construction which shall be kept in position while the parts of machinery required to be fenced are in motion or in use, namely -

(a) every moving part of a prime mover, and every fly wheel connected to a prime mover;

(b) the headrace and tailrace of every water wheel and water turbine;

(c) any part of a stock-bar which projects beyond head stock of a lathe; and

(d) unless they are in such position or of such construction as to be as safe to every person employed in the factory as they would be if they were securely fenced -

(i) every part of an electric generator, a motor or rotary convertor;

(ii) every part of transmission machinery; and

(iii) every dangerous part of any machinery:

Provided that, in the case of dangerous parts of machinery that cannot be securely fenced by reason of the nature of operation, such fencing may by substituted by other adequate measures, such as -

(i) devices automatically preventing the operation from coming into contact with the dangerous parts ; and

(ii) automatic stopping devices :

Provided further that, for the purpose of determining whether any part of machinery is in such position or is of such construction as to be safe as aforesaid, account shall not be taken of any occasion when it being necessary to make an examination of the machinery while it is in motion or, as a result of such examination, to carry out any mounting or shipping of belts, lubrication or other adjusting operation while the machinery is in motion, such examination or operation is made or carried out in accordance with the provisions of section 27.

(2) Without prejudice to any other provisions of this Act relating to the fencing of machinery, every set screw, bolt and key on any revolving shaft, spindle wheel or pinion and all spur, worm and other toothed or friction gearing in motion with which such worker, should otherwise be liable to come into contact, shall be securely fenced to prevent such contact.

(3) The Provincial Government may exempt, subject to such conditions as may be imposed, for securing the safety of the workers, any particular machinery or part from the provisions of this section.

(4) The Provincial Government may, by rules, prescribe such further precautions as it may consider necessary in respect of any particular machinery or part thereof.

27. Work on or near machinery in motion. -

(1) Where in any factory it becomes necessary to examine any part of machinery referred to in section 26 while the machinery is in motion, or as a result of such examination, to carry out any mounting or shipping of belts, lubrication or other adjusting operation while the machinery is in motion, such examination or operation shall be made or carried, out only by a specially trained adult male worker wearing tight fitting clothing whose name has been recorded in the register prescribed in this behalf and while he is so engaged, such worker shall not handle a belt at a moving pulley unless the belt is less than six inches in width and unless the belt joint is either laced or flush with the belt.

(2) No woman or child shall be allowed in any factory to clean, lubricate or adjust any part of machinery while that part is in motion, or to work between moving parts or between fixed and moving parts of any machinery which is in motion.

(3) The Provincial Government may, by notification in the official Gazette, prohibit, in any specified factory or class or description of factories, the cleaning, lubricating or adjusting by any person, of specified parts of machinery when those parts arc in motion.

28. Employment of young persons on dangerous machines. -

(1) No child or adolescent shall work at any machine unless he has been fully instructed as to the dangers arising in connection with the machine and the precautions to be observed and -

(a) has received sufficient training in work at the machine, or

(b) is under adequate supervision by a person who has thorough knowledge and experience of the machine.

(2) This section shall apply to such machines as may be notified by the Provincial Government to be of such a dangerous character that children or adolescents ought not to work at them unless the foregoing requirements are complied with.

29. Striking gear and devices for catting off power. -

(1) In every factory -

(a) suitable striking gear or other efficient mechanical appliances shall be provided and maintained and used to move driving belts to and from fast and loose pulleys which form part of the transmission machinery, and such gear or appliances shall be so constructed, placed and maintained as to prevent the belt from creeping back on the fast pulleys;

(b) driving belts when not in use shall not be allowed to rest or ride upon shafting in motion.

(2) In every factory suitable devices for cutting off power in emergencies from running machinery shall be provided and maintained in every workroom.

(3) In respect of factories in operation before the commencement of this Ordinance the provisions of sub-section (2) shall apply only to workrooms in which electricity is used for power.

30. Self-acting machines. - No traversing part of a self-acting machine in any factory and no material carried thereon shall, if the space over which it runs is a space over which any person is liable to pass whether in the course of his employment or otherwise, be allowed to run on its outward or inward traverse within a distance of eighteen inches from any fixed structure which is not part of the machine :

Provided that the Chief Inspector may permit the continued use of a machine installed before the commencement1 of the Labour Laws (Amendment) Ordinance, 1972, which does not comply with the requirements of this section on such conditions for ensuring safety as he may think fit to impose.

31. Casing of new machinery. -

(1) In all machinery driven by power and installed in any factory after the commencement of the Labour Laws (Amendment) Ordinance, 1972 -

(a) every set screw, belt or key on any revolving shaft, spindle, wheel or pinion shall be so sunk, encased or otherwise effectively guarded as to prevent danger; and

(b) all spur, worm and other toothed or friction gearing which does not require frequent adjustment while in motion shall be completely encased unless it is so situated as to be as safe as it would be if it were completely encased.

(2) Whoever sells or lets on hire or, as agent of a seller or hirer, causes or procures to be sold or let on hire, for use in a factory any machinery driven by power which does not comply with the provisions of sub-section (1), shall be punishable with imprisonment, for a term which may extend to three months, or with fine which may extend to five hundred rupees, or with both.

(3) The Provincial Government may make rules specifying further safeguards to be provided in respect of any other dangerous part of any particular machine or class or description of machines.

32. Prohibition of employment of women and children near cotton openers. - No woman or child shall be employed in any part of a factory for pressing cotton in which a cotton-opener is at work :

Provided that if the feed end of a cotton-opener is in a room separated from the delivery end by a partition extending to the roof or to such height as the Inspector may in any particular case specify in writing, women and children may be employed on the side of the partition where the feed end is situated.

33. Cranes and other lifting machinery. -

(1) The following provisions shall apply in respect of cranes and all other lifting machinery, other than hoists and lifts in any factory : -

(a) every part thereof, including the working gear, whether fixed or movable, ropes and chains and anchoring and fixing appliances shall be -

(i) of good construction, sound material and adequate strength ;

(ii) properly maintained ;

(iii) thoroughly examined by a competent person at least once in every period of twelve months, and a register shall be kept containing the prescribed particulars of every such examination ;

(b) no such machinery shall be loaded beyond the safe working load which shall be plainly marked thereon ;

(c) while any person is employed or working on or near the wheel tract of a travelling crane in any place where he would be liable to be struck by the crane, effective measures shall be taken to ensure that the crane does not approach within twenty feet of that place or come into accidental contact with live electrical lines ;

(d) limit switches shall be provided to prevent over-running ; and

(e) jib cranes, permitting the raising or lowering of the jib shall be provided with an automatic safe load indicator or have attached to them a table indicating the safe working load at corresponding inclinations of the jib.

(2) The Provincial Government may make rules in respect of any lifting machinery or class or description of lifting machinery in factories -

(a) prescribing requirements to be complied with in addition to those set out in this section ; or

(b) exempting from compliance with all or any of the requirements of this section, where in its opinion such compliance is unnecessary or impracticable.

33-A. Hoists and lifts -

(1) In every factory -

(a) every hoist and lift shall be -

(i) of good mechanical construction, sound material and adequate strength;

(ii) properly maintained, and shall be thoroughly examined by a competent person authorised by the Chief Inspector in this behalf at least once in every period of six months, and a register shall be kept containing the prescribed particulars of every such examination of which a copy shall be forwarded to the Chief Inspector;

(b) every hoistway and liftway shall be sufficiently protected by an enclosure fitted with gates, and the hoist or lift and every such enclosure shall be so constructed as to prevent any person or thing from being trapped between any part of the hoist or lift and any fixed structure or moving part;

(c) the maximum safe working load shall be plainly marked on every hoist or lift, and no load greater than such load shall be carried thereon;

(d) the cage of every hoist or lift used for carrying persons shall be fitted with a gate on each side from which access is afforded to a landing;

(e) every gate referred to in clause (b) or clause (d) shall be fitted with interlocking or other efficient device to secure that the gate cannot be opened except when the cage is at the landing and that the cage cannot be moved unless the gate is closed.

(2) The following additional requirements shall apply to hoists and lifts used for carrying persons and installed or reconstructed in a factory after the commencement of the Labour Laws (Amendment) Ordinance, 1972, namely: -

(a) where the cage is supported by rope or chain there shall be at least two ropes or chains separately connected with the cage and balance weight, and each rope or chain with its attachments shall be capable of carrying the whole weight of the cage together with its maximum load ;

(b) efficient devices shall be provided and maintained capable of supporting the cage together with its maximum load in the event of breakage of the ropes, chains or attachments ;

(c) an efficient automatic device shall be provided and maintained to prevent the cage from over-running.

(3) The Chief Inspector may permit the continued use of a hoist or lift installed in a factory before the commencement of this Ordinance which does not fully comply with the provisions of sub-section (1) upon such conditions for ensuring safety as he may think fit to impose.

(4) The Provincial Government may, if in respect of class or description of hoist or lift, it is of opinion that it would be unreasonable to enforce any requirement of sub-sections (1) and (2), by order direct that such requirements shall not apply to such class or description of hoist or lift.

33-B. Revolving machinery -

(1) In every room in a factory in which the process of grinding is carried on there shall be permanently affixed to or placed near each machine in use a notice indicating the maximum safe working peripheral speed of every grind stone or abrasive wheel, the speed of the shaft or spindle upon which the wheel is mounted and the diameter of the pulley upon such shaft or spindle necessary to secure such safe working peripheral speed.

(2) The speeds indicated in the notice under sub-section (1) shall not be exceeded.

(3) Effective measures shall be taken in every factory to ensure that the safe working peripheral speed of every revolving vessel, cage basket, flywheel, pulley, disc or similar appliance, driven by power is not exceeded.

33-C. Pressure plant. -

(1) If in any factory any part of the plant or machinery used in a manufacturing process is operated at a pressure above atmospheric pressure, effective measures shall be taken to ensure that safe working pressure of such part is not exceeded.

(2) The Provincial Government may make rules providing for the examination and testing of any plant or machinery such as is referred to in sub-section (1) and prescribing such other safety measures in relation thereto as may, in its opinion, be necessary in any factory or class or description of factories.

33-D. Floors, stairs and means of access. - In every factory -

(a) all floors, stairs, passages and gangways shall be of sound construction and properly maintained and where it is necessary to ensure safety, steps, stairs, ladders, passages and gangways shall be provided with substantial handrails;

(b) there shall, so far as is reasonably practicable, be provided and maintained safe means of access to every place at which any person is at any time required to work;

(c) all places of work from which a worker may be liable to fall a distance exceeding three feet and six inches shall be provided with fencing or other suitable safeguards; and

(d) adequate provision shall be made for the drainage of floors in wet processes and for the use of slatted stands and platforms.

33-E. Pits, sumps, opening in floors, etc. -

(1) In every factory, every fixed vessel, sump, tank pit or opening in the ground or in floor which by reason of its depth, situation, construction or contents, is or may be a source of danger, shall be either securely covered or securely fenced.

(2) The Provincial Government may, by order in writing, exempt, subject to such conditions as may be imposed, any factory or class or description of factories in respect of any vessel, sump, tank pit or opening from compliance with the provisions of this section.

33-F. Excessive weights. -

(1) No person shall be employed in any factory to lift, carry or move any load so heavy as to be likely to cause him injury.

(2) The Provincial Government may make rules prescribing the maximum weights which may be lifted, carried or moved by adult men, adult women, adolescents and children employed in factories or in carrying on any specified process.

33-G. Protection of eyes. - The Provincial Government may, in respect of any manufacturing process carried on in any factory, by rule require that effective screens or suitable goggles shall be provided for the protection of persons employed on, or in the immediate vicinity of, a process which involves -

(a) risk of injury to the eyes from particles or fragments thrown off in the course of the process, or

(b) risk to the eyes by reason of exposure to excessive light or heat.

33-H. Powers to require specifications of defective parts or tests of stability. - If it appears to the Inspector that any building or any part of the ways, machinery or plant in a factory, is in such a condition that it may be dangerous to human life or safety, he may serve on the Manager of the factory an order in writing, requiring him before a specified date -

(a) to furnish such drawings, specifications and other particulars as may be necessary to determine whether such building, ways, machinery or plant can be used with safety, or

(b) to carry out such tests as may be necessary to determine the strength or quality of any specified parts and to inform the Inspector of the results thereof.

33-I. Safety of building, machinery and manufacturing process. -

(1) If it appears to the Inspector that any building or part of a building or any part of the ways, machinery or plant or manufacturing process in a factory is in such a condition that it is dangerous to human health or safety, he may serve on the Manager of the factory an order in writing specifying the measures which, in his opinion, should be adopted, and requiring them to be carried out before a specified date.

(2) If it appears to the Chief Inspector that the requisitions made under sub-section (1) are not satisfactorily fulfilled thereby involving exposure of workers to serious hazards, he may serve on the Manager of the factory an order in writing, containing a statement of the grounds of his opinion, prohibiting until the danger is removed, the employment, in or about the factory or part thereof, of any person whose employment is not in his opinion reasonably necessary for the purpose of removing the danger.

(3) If it appears to the Inspector that the use of any building or part of a building or of any part of the ways, machinery or plant or manufacturing process in a Factory involves imminent danger to human health or safety he may serve on the Manager of factory an order in writing prohibiting, until the danger is removed, the employment, in or about the factory or part thereof, of any person whose employment is not in his opinion reasonably necessary for the purpose of removing the danger.

(4) Nothing in sub-section (2) or (3) shall be deemed to affect the continuance in the employment of the factory of a person whose employment in or about the factory or part thereof is prohibited under that sub-section.

33- J. Power to make rules to supplement this Chapter. - The Provincial Government may make rules requiring that -

(1) in any factory or in any class or description of factories, such further devices and measures for securing the safety of the persons employed therein as it may deem necessary shall be adopted: and

(2) work on a manufacturing process carried on with the aid of power shall not be begun in any building or part of a building erected or taken into use as a factory until a certificate of stability in the prescribed form and signed by a person possessing the prescribed qualifications has been sent to the Chief Inspector.

33-K. Precautions against dangerous fumes. -

(1) In any factory no person shall enter or be permitted to enter any chamber, tank, vat, pit, pipe, flue or other confined space in which dangerous fumes are likely to be present to such an extent as to involve risk of persons being overcome thereby, unless it is provided with a manhole of adequate size or other effective means of ingress.

(2) No portable electric light of voltage exceeding twenty-four volts shall be permitted in any factory for use inside any confined space such as is referred to in sub-section (1) and, where the fumes present are likely to be inflammable, a lamp or light other than of flame proof construction shall not be permitted to be used in such confined space.

(3) No person in any factory shall enter or be permitted to enter any confined space such as is referred to in sub-section (1) until all practicable measures have been taken to remove any fumes which may be present and to prevent ingress of fumes and unless either -

(a) a certificate in writing has been given by a competent person, based on a test carried out by himself, that the space is free from dangerous fumes and fit for persons to enter, or

(b) the worker is wearing suitable breathing apparatus and a belt securely attached to a rope, the free end of which is held by a person standing outside the confined space.

(4) Suitable breathing apparatus, reviving apparatus and belts and ropes shall in every factory be kept ready for instant use beside any such confined space as aforesaid which any person has entered, and all such apparatus shall be periodically examined and certified by a competent person to be fit for use; and a sufficient number of persons employed in every factory shall be trained and practised in the use of all such apparatus and in the method of restoring respiration.

(5) No person shall be permitted to enter in any factory, any boiler furnace, boiler flue, chamber, tank, vat, pipe or other confined space for the purpose of working or making any examination therein until it has been sufficiently cooled by ventilation or otherwise to be safe for persons to enter.

(6) The Provincial Government may make rules prescribing the maximum dimensions of the manholes referred to in sub-section (1) and may, by order in writing, exempt, subject to such conditions as it may think fit to impose, any factory or class or description of factories from compliance with any of the provisions of this section.

33-L. Explosive or inflammable dust, gas, etc. -

(1) Where in any factory any manufacturing process produces dust, gas, fume or vapour of such character and to such extent as to be likely to explode on ignition, all practicable measures shall be taken to prevent any such explosion by -

(a) effective enclosure of the plant or machinery used in the process ;

(b) removal or prevention of the accumulation of such dust, gas, fume or vapour ;

(c) exclusion or effective enclosure of all possible sources of ignition.

(2) Where in any factory the plant or machinery used in a process such as is referred to in sub-section (1) is not so constructed as to withstand the probable pressure which such an explosion as aforesaid would produce, all practicable measures shall be taken to restrict the spread and effects of the explosion by the provision in the plant or machinery of chokes, baffles, vents or other effective appliances.

(3) Where any part of the plant or machinery in a factory contains any explosive or inflammable gas or vapour under pressure greater than atmospheric pressure, that part shall not be opened except in accordance with the following provisions, namely: -

(a) before the fastening of any joint of any pipe connected with the part of the fastening of the cover of any opening into the part is loosened, any flow of the gas or vapour into the part or any such pipe shall be effectively stopped by a stop-valve or other means;

(b) before any such fastening as aforesaid is removed all practicable measures shall be taken to reduce the pressure of the gas or vapour in the part or pipe to atmospheric pressure ;

(c) where any such fastening as aforesaid has been loosened or removed, affective measures shall be taken to prevent any explosive or inflammable gas or vapour from entering the part or pipe until the fastening has been secured, or, as the case may be, securely replaced;

Provided that the provisions of sub-section shall not apply in the case of plant or machinery installed in the open air.

(4) No plant, tank or vessel which contains or has contained any explosive or inflammable substance shall be subjected in any factory to any welding, brazing, soldering or cutting operation which involves the application of heat or to any drilling or other operation which is likely to create heat or sparks, unless adequate measures have first been taken to remove such substance and any fumes arising therefrom or to render such substance and fumes non-explosive or non-inflammable, and no such substance shall be allowed to enter such plant, tank or vessel after any such operation until the metal has cooled sufficiently to prevent any risk of igniting the substance.

(5) The Provincial Government may by rules exempt, subject to such conditions as may be prescribed, any factory or class or description of factories from compliance with all or any of the provisions of this section.

33-M. Power to exclude children. -

(1) The Provincial Government may make rules prohibiting the admission to any specified class of factories, or to specified parts thereof, of children who cannot be lawfully employed therein.

(2) If it appears to the Inspector that the presence in any factory or part of a factory of children who cannot be lawfully employed therein may be dangerous to them or injurious to their health, he may serve on the manager of the factory an order in writing directing him to prevent the admission of such children to the factory or any part of it.

33-N. Notice of certain accidents. - Where in any factory an accident occurs which causes death, or which causes any bodily injury whereby any person injured is prevented from resuming his work in the factory during the forty-eight hours after the accident occurred, or which is of any nature which may be prescribed in this behalf, the manager of the factory shall send notice thereof to such authorities, and in such form and within such time, as may be prescribed.

33-P. Appeals. -

(1) The manager of a factory on whom an order in writing by an Inspector has been served under the provisions of this Chapter, or the occupier of the factory, may, within thirty days of service of the order, appeal against it to the Provincial Government, or to such authority as the Provincial Government may appoint in this behalf, and the Provincial Government or appointed authority may, subject to rules made in this behalf by the Provincial Government, confirm, modify or reverse the order.

(2) The appellate authority may, and if so required in the petition or appeal shall, bear the appeal with the aid of assessors, one of whom shall be appointed by the appellate authority and the other by such body representing the industry concerned as the Provincial Government may prescribe in this behalf:

Provided that if no assessor is appointed by such body, or if the assessor so appointed fails to attend at the time and place fixed for hearing the appeal, the appellate authority may, unless satisfied that the failure to attend is due to sufficient cause, proceed to hear the appeal without the aid of such assessor, or if it thinks fit, without the aid of any assessor.

(3) Except in the case of an appeal against an order under sub-section (3) of section 33-I or sub-section (2) of section 33-M, the appellate authority may suspend the order appealed against pending the decision of the appeal, subject however to such conditions as to partial compliance or the adoption of temporary measures as it may choose to impose in any case.

33-Q. Additional power to make health and safety rules relating to shelters during rest. -

(1) The Provincial Government may make rules requiring that in any specified factory wherein more than one hundred and fifty workers are ordinarily employed, an adequate shelter shall be provided for the use of workers during periods of rest, and such rules may prescribe the standards of such shelters.

(2) Rooms for children. - The Provincial Government may also make rules

(a) requiring that in any specified factory, wherein more than fifty women workers are ordinarily employed, a suitable room shall be reserved for the use of children under the age of six years belonging to such women, and

(b) prescribing the standards for such rooms and the nature of the supervision to be exercised over the children therein.

(3) Certificates of stability. - The Provincial Government may also make rules, for any class of factories and for the whole or any part of the Province, requiring that work on a manufacturing process carried on with the aid of power shall not be begun in any building or part of a building erected or taken into use as a factory after the commencement of this Act, until a certificate of stability in the prescribed form, signed by a person possessing the prescribed qualifications, has been sent to the Inspector.

(4) Hazardous operations. - Where the Provincial Government is satisfied that any operation in a factory exposes any persons employed upon it to a serious risk of bodily injury, poisoning or disease, it may make rules applicable to any factory or class of factories in which the operation is carried on -

(a) specifying the operation and declaring it to be hazardous,

(b) prohibiting or restricting the employment of women, adolescents or children upon the operation,

(c) providing for the medical examination of persons employed or seeking to be employed upon the operation and prohibiting the employment of persons not certified as fit for such employment, and

(d) providing for the protection of all persons employed upon the operation or in the vicinity of the places where it is carried on.

(5) The Provincial Government may also make rules requiring the occupiers or managers of factories to maintain stores of First-Aid appliances and provide for their proper custody and use.

13. Cleanliness. -

(1) Every factory shall be kept clean and free from effluvia arising from any drain, privy or other nuisance, and in particular, -

(a) accumulation of dirt and refuse shall be removed daily by sweeping or by any other effective method from the floors and benches of work-rooms and from staircases and disposed of in a suitable manner ;

(b) the floor of every work-room shall be cleaned at least once in every week by washing, using disinfectant where necessary or by some other effective method ;

(c) where the floor is liable to become wet in the course of any manufacturing process to such extent as is capable of being drained, effective means of drainage shall be provided and maintained ;

(d) all inside walls and partitions, all ceilings, or tops of rooms and walls, sides and tops or passages and staircases shall -

(i) where they are painted or varnished, be repainted or revarnished at least once in every five years ;

(ii) where they arc painted or varnished and have smooth impervious surfaces, be cleaned at least once in every fourteen months, by such methods as may be prescribed ;

(iii) in any other case, kept whitewashed or colour washed and the whitewashing or colour washing shall be carried out at least once in every fourteen months ; and

(e) the dates on which the processes required by clause (d) are carried out shall be entered in the prescribed register.

(2) If, in view of the nature of the operations carried on in a factory it is not possible for the occupier to comply with all or any of the provisions of sub-section (1), the Provincial Government may, by an order, exempt such factory or class or description of factories from any of the provisions of that sub-section and specify alternative methods for keeping the factory in a clean state.

14. Disposal of wastes and effluents. -

(1) Effective arrangements shall be made in every factory for the disposal of wastes and effluents due to the manufacturing process carried on therein.

(2) The Provincial Government may make rules prescribing the arrangements to be made under sub-section (1) or requiring that the arrangements made in accordance with that sub-section shall be subject to the approval of such authority as may be prescribed.

15. Ventilation and temperature. -

(1) Effective and suitable provisions shall be made in every factory for securing and maintaining in every work-room -

(a) adequate ventilation by the circulation of fresh air, and

(b) such temperature as will secure to workers therein reasonable conditions of comfort and prevent injury to health, and in particular -

(i) the walls and roofs shall be of such material and so designed that such temperature shall not be exceeded but kept as low as practicable ;

(ii) where the nature of the work carried on in the factory involves, or is likely to involve, the production of excessively high temperature, such adequate measures as are practicable shall be taken to protect the workers therefrom by separating the process which produces such temperature from the work-room by insulating the hot parts or by other effective means.

(2) The Provincial Government may prescribe a standard of adequate ventilation and reasonable temperature for any factory or class or description of factories or parts thereof and direct that a thermometer shall be provided and maintained in such place and position as may be specified.

(3) If it appears to the Provincial Government that in any factory or class or description of factories excessively high temperature can be reduced by such methods as whitewashing, spraying or insulating and screening outside walls or roofs or windows, or by raising the level of the roof, or by insulating the roof either by an air space and double roof or by the use of insulating roof materials, or by other methods, it may prescribe such of these or other methods to be adopted in the factory.

16. Dust and fume. -

(1) In every factory in which, by reason of the manufacturing process carried on, there is given off any dust or fume or other impurity of such a nature and to such an extent as is likely to be injurious or offensive to the workers employed therein, effective measures shall be taken to prevent its accumulation in any work-room and its inhalation by workers and if any exhaust appliance is necessary for this purpose, it shall be applied as near as possible to the point of origin of the dust, fume or other impurity, and such point shall be enclosed so far as possible.

(2) In any factory no stationary internal combustion engine shall be operated unless the exhaust is conducted into open air and exhaust pipes are insulated to prevent scalding and radiation heat, and no internal combustion engine shall be operated in any room unless effective measures have been taken to prevent such accumulation of fumes therefrom as are likely to be injurious to the workers employed in the work-room.

17. Artificial humidification. -

(1) The Provincial Government may, in respect of all factories in which humidity of the air is artificially increased, make rules -

(a) prescribing standards of humidification ;

(b) regulating the methods used for artificially increasing the humidity of the air ;

(c) directing prescribed tests for determining the humidity of the air to be correctly carried out and recorded, and

(d) prescribing methods to be adopted for securing adequate ventilation and cooling of the air in the work-rooms.

(2) In any factory in which the humidity of the air is artificially increased, the water used for the purpose shall be taken from a public supply, or other source of drinking water, or shall be effectively purified before it is so used.

(3) If it appears to an Inspector that the water used in a factory for increasing humidity which is required to be effectively purified under sub-section (2) is not effectively purified, he may serve on the Manager of the factory an order in writing specifying the measures which, in his opinion, should be adopted, and requiring them to be carried out before a specified date.

18. Overcrowding. -

(1) No work-room in any factory shall be over-crowded to an extent injurious to the health of the workers employed therein.

(2) Without prejudice to the generality of the provisions of sub-section (1) there shall be provided for every worker employed in a work-room -

(a) at least three hundred and fifty cubic feet of space in the case of a factory in existence on the date of the commencement1 of the Labour Laws (Amendment) Ordinance, 1972; and

(b) at least five hundred cubic feet of space in the case of a factory built after the commencement of the Labour Laws (Amendment) Ordinance, 1972.

Explanation. - For the purpose of this sub-section no account shall be taken of a space which is more than fourteen feet above the level of the floor of the room.

(3) If the Chief Inspector by order in writing so requires, there shall be posted in each work-room of a factory a notice specifying the maximum number of workers who may in compliance with the provisions of this section be employed in the room.

(4) The Chief Inspector may, by order in writing, exempt, subject to such conditions as he may think fit to impose, any work-room from the provisions of this section if he is satisfied that compliance therewith in respect of such room is not necessary for the purpose of health of the workers employed therein.

19. Lighting. -

(1) In every part of a factory where workers are working or passing, there shall be provided and maintained -

(a) sufficient and suitable lighting, natural or artificial, or both; and

(b) emergency lighting of special points in work-room and passages to function automatically in case of a failure of the ordinary electric system.

(2) In every factory all glazed windows and sky-lights used for the lighting of the work-room shall be kept clean on both the outer and inner surfaces and free from obstruction as far as possible under the rules framed under sub-section (3) of section 15.

(3) In every factory effective provisions shall, so far as is practicable, be made for the prevention of -

(a) glare either directly from any source of light or by reflection from a smooth or polished surface; and

(b) the formation of shadows to such an extent as to cause eye strain or risk of accident to any worker.

(4) The Provincial Government may prescribe standards of sufficient and suitable lighting for factories or for any class or description of factories or for any manufacturing process.

20. Drinking Water. -

(1) In every factory effective arrangements shall be made to provide and maintain at suitable points conveniently situated for all workers employed therein a sufficient supply of whole-some drinking water.

(2) All such points shall be legibly marked "Drinking Water" in a language understood by the majority of the workers and no such point shall be situated within twenty feet of any washing place, urinal or latrine, unless a shorter distance is approved in writing by the Chief Inspector.

(3) In every factory wherein more than two hundred and fifty workers are ordinarily employed, provision shall be made for cooling the drinking water during the hot weather by effective means and for distribution thereof and arrangements shall also be made for -

(a) the daily renewal of water if not laid on; and

(b) a sufficient number of cups or other drinking vessels, unless the water is being delivered in an upward jet.

(4) The Provincial Government may, in respect of all factories or any class or description of factories, make rules for securing compliance with the provisions of this section.

21. Latrines and urinals. -

(1) In every factory -

(a) sufficient latrines and urinals of prescribed types shall be provided conveniently situated and accessible to workers at all times while they are in the factory;

(b) enclosed latrines and urinals shall be provided separately for male and female workers;

(c) such latrines and urinals shall be adequately lighted and ventilated and no latrine and urinal shall, unless specially exempted in writing by the Chief Inspector, communicate with any workroom except through an intervening open space or ventilated passage;

(d) all such latrines and urinals shall be maintained in a clean and sanitary condition at all times with suitable detergents or disinfectants or with both;

(e) the floors and internal walls of the latrines and urinals and the sanitary blocks shall, up to a height of three feet, be finished to provide a smooth polished impervious surface; and

(f) washing facilities shall be provided near every sanitary convenience.

(2) The Provincial Government may prescribe the number of latrines and urinals to be provided in any factory in proportion to the number of male and female workers ordinarily employed therein and such further matters in respect of sanitation in the factories as it may deem fit.

22. Spittoons. -

(1) In every factory there shall be provided, at convenient places, a sufficient number of spittoons which shall be maintained in a clean and hygienic condition.

(2) The Provincial Government may make rules prescribing the type and the number of spittoons to be provided and their location in any factory and such further matters as may be deemed necessary relating to their maintenance in a clean and hygienic condition.

(3) No person shall spit within the premises of a factory except in the spittoons provided for the purpose. A Notice containing this provision and the penalty for its violation shall be prominently displayed at suitable places in the premises.

(4) Whosoever spits in contravention of sub-section (3) shall be punishable with a fine not exceeding two rupees.

23. Precautions against contagious or infections disease. -

(1) Each worker in a factory shall be provided with a "Hygiene Card' in which during the month of January and July every year entries shall be recorded after examination by appointed factory doctor to the effect that the worker is not suffering from any contagious or infectious disease. The fee of such an examination shall be fixed by the Provincial Government and will be borne by the occupier or manager of the factory.

(2) If a worker is found to be suffering from any contagious or infectious disease on an examination under sub-section (1), he shall not be appointed on work till he is declared free of such a disease.

23-A. Compulsory vaccination and inoculation. - Each worker in a factory shall be vaccinated and inoculated against such diseases and at such intervals as may be prescribed. The expenses, if any, of such vaccination and inoculation shall be borne by the occupier or manager of the factory.

24. Power to make rules for provision of canteens. -

(1) The Provincial Government may make rules requiring that in any specified factory wherein more than two hundred and fifty workers are ordinarily employed, an adequate canteen shall be provided for the use of the workers.

(2) Without prejudice to the generality of the foregoing power, such rules may provide for -

(a) the date by which such canteen shall be provided;

(b) the standards in respect of construction, accommodation, furniture and other equipment of the canteen;

(c) the foodstuffs to be served therein and the charges which may be made therefor;

(d) representation of the workmen in the management of the canteens;

(e) enabling, subject to such conditions, if any, as may be specified, the power to make rules under clause (c) to be exercised also by the Chief Inspector.